Online Resources

Discussion by economist Joel Slemrod noting that the most detailed study ever done on American tax burdens, by Joseph Pechman in 1984, indicated that whether those at the top or bottom end of the income scale pay a higher percentage of their incomes in total taxes depends on the assumption used of who bears the ultimate burden of corporate taxation:

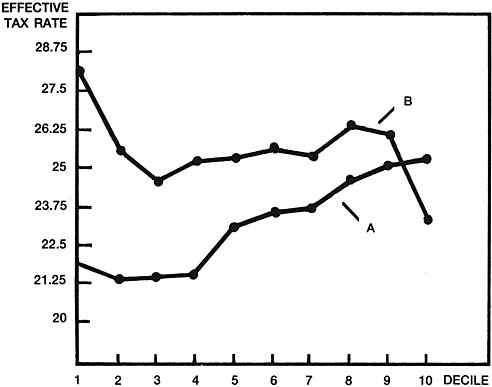

CHART1 illustrates the progressivity of the overall U.S. tax system in 1985 (the latest year for which this information is available), according to two different assumptions about the shifting of taxes. Under assumption A the average tax rate generally increased with income, suggesting a generally progressive tax. Under assumption B the average tax rate actually is lowest for families in the highest income decile. The key difference between the two results is that B assumes that half of the corporation income tax is shifted to consumers, in the form of higher prices, while A assumes that all of it is borne by shareholders, who are generally high-income taxpayers. Chart 1 illustrates both the importance of the shifting assumptions and the fact that, even though the federal income tax by itself is progressive, its progressivity is overwhelmed by less progressive levies such as sales taxes and, to a lesser extent, the payroll tax.

Chart 1. Effective Tax Rate by Income Decile, 1985

SOURCE: Graph from Stiglitz, p. 348, based on Pechman, 1985.

University of Michigan Business School Office of Tax Policy and Research

Center on Budget and Policy Priorities

Fiscal advocacy for moderate-to-lower incomes.

Citizens for Tax Justice

Tax advocacy group.

Critiques of Libertarianism

Mike Huben compiles critiques of libertarian anti-taxation arguments.

Economics 127 Public Finance: Taxation Syllabus

Dr. Deborah Garvey of Santa Clara University’s syllabus points to several useful resources.

Econ 315: Public Economics

University of Missouri.

Washington Post Tax Policy

Urban-Brookings Tax Policy Center

“Provides timely, accessible analysis and facts about tax policy to policymakers, journalists, citizens, and researchers.”

President's Advisory Panel on Federal Tax Reform

Joint Committee on Taxation

Taxing Thoughts

Debate Stream

1996

6/23

Cutting Taxes Could Also Cut Growth

William Gale of Brookings expounds on the risks of certain tax-cutting policy mixes.

1999

1/21

Information and Misinformation about Federal Tax Burdens

A Center on Budget and Policy Priorities brief rebutting Tax Foundation numbers on median family tax burdens.

2/24

Are Americans Really Overtaxed?

William Gale outlines issues of tax burdens.

March

The Case Against Tax Cuts

William Gale briefly surveys tax burdens in this Brookings Institute Policy Brief.

2000

8/20

Most Unkindest Cuts

Paul Krugman distills the difference between the two party’s income tax proposals and counters the Wall Street Journal’s recycling of the University of Michigan study.

8/23

Al Gore’s Class Warfare

Bruce Bartlett responds to Krugman (by citing the Michigan and Dallas Fed studies.)

2001

2/12

The Rich Get Richer

Edward Wolff, writing in the American Prospect , enumerates proposals to alleviate the effects of income and wealth inequality.

6/1

Tax Policy From 1990 to 2001[PDF]

A review by Eugene Steuerle of the Urban Institute.

6/11

Tax Burden Rising for the Rich and Not So Rich

Bruce Bartlett, writing for the Pete Dupont-founded National Center for Policy Analysis, responds in an assessment of the tax rates on the top 5%.

2002

4/10

Overall Federal Tax Burden on Most Families — Including Middle-Income Families — at Lowest Levels in More Than Two Decades: Income Taxes for Median Family of Four at Lowest Level in 44 Years

An update on middle-class tax burdens from the verbose Center on Budget and Policy Priorities.

9/19

Alternative Minimum Tax

Brad DeLong introduces a New York Times article outlining the effects of the Bush tax cut on the middle class.

10/31

Do Lower Taxes Mean Faster Economic Growth?

Jeff Madrick, writing in The New York Times, surveys the empirical evidence against long-run stimulative effects of tax cuts.

11/7

Whinging and Snivelling From a Democrat

Brad DeLong, writing in his Semi-Daily Journal, lays out a theoretical basis for efficacious Republican tax policy:

· ... Let me give you some marginal tax rates... a mother with two kids earning $24000: 68% (she loses the last of her food stamps, and her earned income tax credit phases out)... a doctor making $200,000: 36.4%... an executive making $1,000,000: 40%... Any decent supply-sider would say that the real place where marginal tax rates needed to be cut in 2001 was around the $25000 a year zone: the place where the phase out of the earned income credit makes marginal rates astronomical. We economist types were never able to interest Clinton and company in such a proposal--at a gut level, Clinton simply didn't get the importance of lower marginal rates so that people don't get hit in the nose by a 2 x 4 when they work more hours and the IRS snarfs most of it. Larry Lindsey is supposed to have led a charge to get a proposal to "deal with the EITC phaseout problem" into the 2001 tax bill, but he got absolutely nowhere. Bush, Cheney, and their personal staffs don't resonate with the problems of mothers of two making $12 an hour... mothers of two making $12 an hour don't give big to Republican presidential candidates, or show up at the $1000 a plate dinners that are what presidential candidates do day after day these days. So we got a tax cut that gives 40% of its notional dollars to those making more than $300,000 a year whose marginal tax rates are much lower than those of the mother of two earning $12 an hour. (Larry Lindsey keeps saying that they'll come back to it and fix it; but the word is that he's about to get "invited" to "spend more time with his family.")12/8

If Tax History Is a Guide, the Poor Are in Trouble

Roger Altman surveys the Republican Party’s historical antipathy to tax relief for those with lower incomes, and notes that a Brookings study by Joseph Pechman in the 1980s indicated that the totality of the American tax system does not effectively change the state of income distribution.

2005

Toward Fundamental Tax Reform [PDF]

AEI publication including Joel Slemrod and others.

4/12

Guest Viewpoint: Some taxation principles, to get debate started

An Op-ed in the Register-Guard by University of Oregon economist Mark Thoma on distributive equity and its application in normative arguments about taxation.

5/5

What Should a Reconfigured Tax System Look Like?

Economist Hal Varian.

7/10

SPINNING THE MYTH....

Kevin Drum on the dearth of family farms paying the Estate tax.

8/15

A Flat Tax Recipe for Disaster

Mark Thoma, at his blog Economist's View, on the latest Steve Forbes column.

10/18

Tax Reform

Kash at the blog Angry Bear links to New York Times coverage of Bush's tax advisory commission and mulls over tax simplification.

2011

8/14

Stop Coddling the Super-Rich

Warren Buffett's classic New York Times op-ed:

Last year my federal tax bill — the income tax I paid, as well as payroll taxes paid by me and on my behalf — was $6,938,744. That sounds like a lot of money. But what I paid was only 17.4 percent of my taxable income — and that’s actually a lower percentage than was paid by any of the other 20 people in our office. Their tax burdens ranged from 33 percent to 41 percent and averaged 36 percent.2012

If you make money with money, as some of my super-rich friends do, your percentage may be a bit lower than mine. But if you earn money from a job, your percentage will surely exceed mine — most likely by a lot.

To understand why, you need to examine the sources of government revenue. Last year about 80 percent of these revenues came from personal income taxes and payroll taxes. The mega-rich pay income taxes at a rate of 15 percent on most of their earnings but pay practically nothing in payroll taxes. It’s a different story for the middle class: typically, they fall into the 15 percent and 25 percent income tax brackets, and then are hit with heavy payroll taxes to boot.

1/19

Corporate Taxes And The .01 Percent

Paul Krugman on the implications on imputing the corporate tax burden to shareholders:

2014On the question of how profits taxation plays into tax burdens, the CBO has already done those calculations. In particular, it did a special version of its usual tax shares analysis that looked inside the top 0.01 percent, taking the data up through 2005 (pdf). According to this analysis, in 2005 the top .01 percent paid only 17 percent of income in income taxes — but they faced an overall federal tax rate of 31.5 percent, with almost all the difference being imputed corporate taxes.But is this really where the right wants to go? I thought corporations were people — by which Romney meant not that they eat and sleep, but that they employ people, and by being nice to corporations we’re being nice to workers. If you say instead that corporate profits benefit only the stockholders — which is what you’re implicitly saying if you impute all profits taxes to the stockholders — so much for the warm and fuzzy feelings.

5/5

Unequal to the Task

In the National Review, Joshua Hendrickson of the University of Mississippi reviews Thomas Piketty's book Capital:

Piketty’s policy solution is logically consistent with his concern regarding the growing importance of inheritance, but it is inadequate. A better conceptual framework for devising tax policy — and one that is consistent with the theoretical literature in this field — would be the following: Some people are born to wealthy parents, and others are born to poor parents. This is what is known as an “idiosyncratic risk.” The government might want a tax policy that insures individuals against this risk; this would tend to be a policy that has high taxes on inheritance. On the other hand, high taxes would discourage the accumulation of wealth. The government therefore must balance the desire to insure individuals against the lottery of birth with the desire to encourage the most productive members of society to be as productive as possible and, in the process, accumulate wealth.

The implications of this framework are at odds with the policy solutions that Piketty suggests. Specifically, while this framework suggests that the optimal tax on inheritance should be progressive, it also implies that the marginal tax rate should be negative. In other words, the optimal tax policy for inheritance is to subsidize inheritance and to reduce the size of the subsidy with the size of the inheritance. It is easy to understand the intuition behind this conclusion: Subsidizing inheritance prevents the deterrent effect of taxation, and the greater subsidization of inheritance for children of poor parents reduces the risks associated with birth.

No comments:

Post a Comment